SpaceX: You Are the Exit Liquidity

Two index committees read the same SpaceX filing. One rewrote its rulebook. One refused. The spread between those two decisions is the only mispricing that matters this week.

TL;DR

- SpaceX prices Thursday, June 11, and starts trading Friday, June 12, as SPCX: $135 a share, $75 billion raised, a $1.75 trillion valuation. The largest IPO in history, at 94 times trailing revenue.

- The filing says what the photos don’t. SpaceX registered as a data processing company. Starlink’s $4.4 billion segment profit funds a $657 million launch loss and a $6.4 billion AI loss. 61 percent of capex goes to AI.

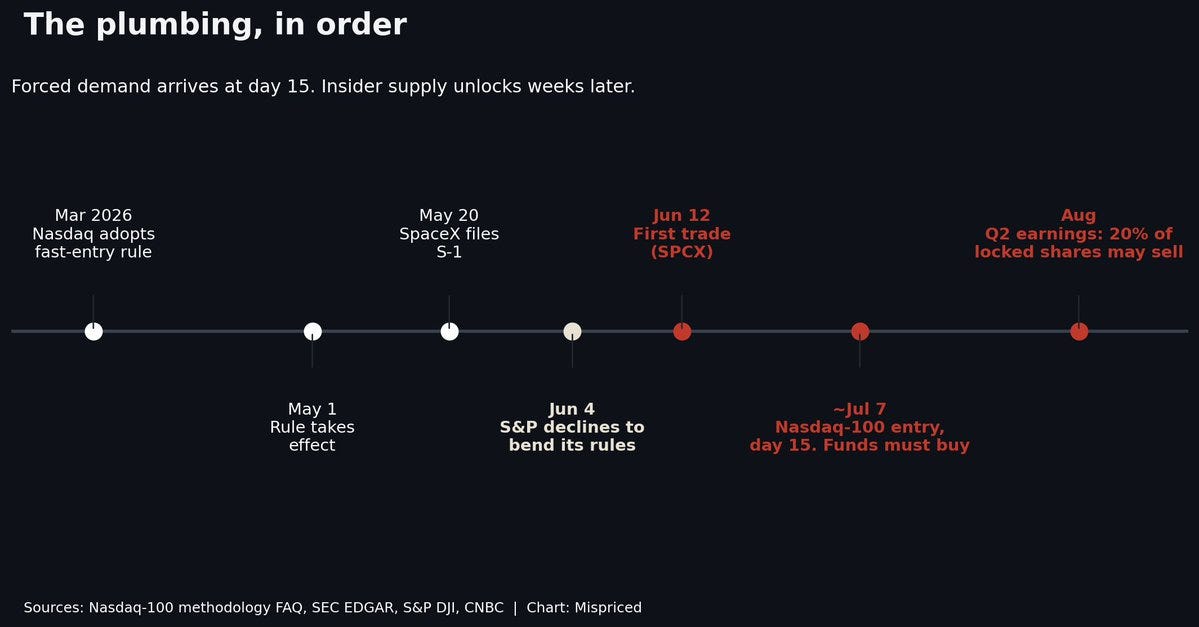

- Nasdaq rewrote its index rules effective May 1: entry 15 trading days after an IPO, no minimum float, and a 3x weight multiplier for low-float names. S&P reviewed the same idea and refused. Only one of them can be right.

- Roughly $5 to 6 billion of forced index buying arrives around July 7. Insider lock-ups release weeks later, in tranches that grow the float and raise the index weight, which forces more buying. The plumbing fits together without a gap.

- The S-1 books the Anthropic compute deal as $45 billion through 2029. Musk publicly calls it a 180-day arrangement. Both reference the same contract.

- The mispricing is not the rocket. It is the rules rewritten to deliver the rocket into your index fund.

---

On June 4, S&P Dow Jones Indices rejected its own idea. The proposal would have done two favors for giant IPOs: cut the waiting period before index entry from twelve months to six, and waive the rule that a company must be profitable. S&P asked market participants what they thought. Then it walked the whole thing back. The rejection ran one sentence, with a knife inside it: exceptions should not be granted, the committee wrote, solely based on market capitalization.

Five weeks earlier, Nasdaq went the other way. Effective May 1, its revised Nasdaq-100 methodology allows any newly listed company ranked in the top 40 by market capitalization to enter the index after 15 trading days. The old minimum free float requirement of 10 percent was eliminated outright. The seasoning period that existed for price discovery is gone for companies of sufficient size.

SpaceX prices its IPO on Thursday, June 11, and trades Friday, June 12, under the ticker SPCX, at $135 per share, 555.6 million shares, a $75 billion raise, a $1.75 trillion valuation. The largest IPO in history, listed on the exchange that changed its rules in time to receive it.

Most coverage this week is arguing about whether SpaceX is worth $1.75 trillion. Morningstar says $780 billion. Damodaran says $1.3 trillion. The S-1 says whatever a 94 times multiple on trailing revenue says. That debate is loud, public, and already in the price of the argument.

The quieter question is structural. When two committees apply different rules to the same security, one of them is wrong, and the capital that tracks the wrong one pays for it mechanically, on a schedule, without anyone making a decision. That is the setup. Here is the filing underneath it.

The plumbing, in order. Sources: Nasdaq-100 methodology FAQ, SEC EDGAR, S&P DJI, CNBC.

One profitable business, wearing two unprofitable ones

Start with the industry code. SpaceX filed its S-1 under SIC 7370: Services, Computer Programming, Data Processing. Not aerospace. Not defense. The company that launches more than 80 percent of global payload mass classified itself, for regulatory purposes, as a data processing company. The first 18 pages of the prospectus are rocket photographs. The industry code is the honest part.

The segment disclosures, public for the first time, explain why. SpaceX is three businesses with opposite financial signatures, recast after the February 2026 all-stock acquisition of xAI, which had itself absorbed X in March 2025.

Connectivity is the engine. Starlink generated $11.4 billion of revenue in 2025, up 49.8 percent, with $4.4 billion of segment operating income at roughly 63 percent adjusted EBITDA margins. Subscribers doubled from 4.4 million to 8.9 million during 2025 and crossed 10.3 million by early 2026. It is the only segment that makes money. It produced effectively all of the consolidated EBITDA.

Space is a platform investment. The launch business posted $4.1 billion of 2025 revenue and a $657 million operating loss, with roughly $3 billion of Starship R&D consuming the cost base. Falcon 9 itself is profitable. The segment is not.

AI is the sink. The xAI segment lost $6.36 billion from operations in 2025 and absorbed $12.7 billion of capital expenditure, 61 percent of the company’s $20.7 billion total capex. In the first quarter of 2026 the pattern held: Connectivity earned $1.19 billion in operating profit, Space lost $619 million, AI lost $2.47 billion. Consolidated Q1 net loss: $4.3 billion. Q1 capex alone ran $10.1 billion, of which $7.7 billion was AI. At that pace, SpaceX will spend more on capex in 2026 than it generated in revenue in 2025.

Segment operating income, FY2025. Data: SpaceX Form S-1.

Morningstar’s framing is the correct one: Starlink’s success is effectively subsidizing xAI’s expenditures. Investors who want the satellite business, and there are good reasons to want it, are required to swallow the AI segment to get it. The AWS-inside-Amazon comparison circulating this week flatters the structure. Amazon’s retail business was not burning six billion dollars a year when AWS emerged.

Capital expenditure by destination. Data: SpaceX Form S-1 and Q1 2026 disclosures.

The related-party disclosures complete the picture. SpaceX spent $131 million on Cybertrucks in 2025 and $697 million on Tesla battery storage systems across 2024 and 2025, at retail. Musk holds 93.6 percent of the Class B shares, which carry ten votes each, giving him 85 percent of voting power on 42 percent of the equity. SpaceX is opting out of Nasdaq’s independent board requirement as a controlled company. The compensation plan ties new Musk equity awards to milestones up to and including a Mars colony.

The valuation debate takes all of this as input and produces a number. Fine. The number is not the story.

Three answers to one question. Sources: Morningstar; Aswath Damodaran via WSJ; SpaceX S-1.

The plumbing

Here is what changed at Nasdaq, specifically, and when.

In March 2026, with SpaceX, Anthropic, and OpenAI all expected to list within the year, Nasdaq adopted a new fast entry rule for the Nasdaq-100, effective May 1. Three revisions matter.

First, speed. A newly listed company ranked in the top 40 by market capitalization becomes index-eligible 15 trading days after its IPO. The prior path ran through annual reconstitution in December, with a three to twelve month seasoning period that existed, in the words of one Wall Street critic, so the market could establish real price discovery before passive investors were forced in.

Second, float. The old methodology excluded securities with less than 10 percent free float. The new methodology has no minimum at all. Instead, a security with float below 20 percent gets its index market capitalization set at three times its float value, capped at 100 percent. Read that mechanism against SpaceX’s offering: roughly 4 to 5 percent of shares floated at IPO, insiders controlling the rest. The multiplier inflates SpaceX’s effective benchmark weight well beyond what its tradable share base supports.

Third, scope. Eligibility and ranking now consider the entire market capitalization, listed and unlisted shares together. A company can be weighted against a share count the public cannot trade.

FTSE Russell adjusted as well; SpaceX is already eligible for Russell inclusion. S&P alone declined, which means S&P 500 trackers sit out for at least a year while Nasdaq-100 and Russell trackers are required to buy.

The size of the requirement is calculable. Roughly $527 billion sat in 63 ETFs tracking the Nasdaq-100 as of December, per ETFGI, before counting structured products and proprietary indices built on top of it. At an initial weight near one percent, inclusion generates approximately $5 to 6 billion of mechanical demand, per the math laid out by heise’s analysis of the methodology FAQ. Those funds must sell Apple, Microsoft, and Nvidia, pro rata, to fund the purchase. No analyst forms a view. The index decides, around July 7, fifteen trading days after Friday.

A reasonable person asks why an exchange would do this. The commercial answer is that exchanges compete for listings, the decade’s largest listings are richly valued private companies with small floats and no GAAP profits, and an index seat is a product feature. The timing has prompted commentators to ask whether the rule change was a marketing play for the exchange business. Nasdaq has not characterized it that way. The sequence of dates is in the public record either way: rule adopted March, effective May 1, SpaceX chose Nasdaq, lists June 12.

The release valves

The standard IPO lock-up bars insider sales for 180 days. SpaceX replaced it with a staircase.

Per the S-1, after the company reports earnings for the quarter through June, its first as a public company, insiders may sell up to 20 percent of their eligible locked shares. Further tranches release on additional triggers. CNBC’s read of the structure is the polite one: phased selling prevents a single cliff where everyone exits at once. The less polite read follows immediately after in the same article. The staircase grows the float, and a growing float raises SpaceX’s index weight under the new low-float weighting rules, which compels tracking funds to buy more, on a schedule, into the insider selling.

Hold the two mechanisms next to each other. Forced passive demand arrives 15 trading days after the IPO. Insider supply unlocks weeks later, in tranches, each tranche raising the index weight and summoning the next round of forced demand. Supply has been engineered to arrive precisely when the buyers who cannot say no show up. Whether by design or coincidence, the plumbing fits together without a gap.

Who is selling into that demand is also in the record. The xAI merger in February converted xAI equity, which had absorbed X’s equity in 2025, which had absorbed the Twitter acquisition’s losses before that, into SpaceX shares. The early backers of a $44 billion social media purchase that lost most of its value now hold stock in a $1.75 trillion company, with a staircase out, and a buyer of last resort that is legally required to show up. That sentence describes the mechanics. It does not require a villain. It only requires the rules as written.

The consensus exhibit, and the caveat the consensus skips

The most circulated chart of the week comes from Truist’s Keith Lerner, who compiled the first-year record of 30 major tech IPOs. The medians: up 3 percent after one week, down 9 percent after twelve months, with only 43 percent of names positive a year out. The column that matters is the last one. Median first-year maximum drawdown: negative 54 percent. Every one of the 30 names drew down. The best case was Okta at negative 20. Robinhood reached negative 90. Meta, the closest analog as a giant consumer-facing IPO with a control structure, fell 54 percent inside year one before becoming one of the great compounders of the era. The exhibit follows, attributed to Truist. We did not compute it; we verified its headline figures against independent coverage.

Year 1 maximum drawdown, 30 major tech IPOs. Data: Truist Advisory Services (Keith Lerner), June 2026, via @saxena_puru

Now the caveat, because this table is on every finance site this week and the herd is reading it one way. Jay Ritter’s IPO research, the academic standard for this question, finds that long-run IPO underperformance concentrates in the smallest companies. Large IPOs, on average, neither outperform nor underperform after their first day. SpaceX is the largest IPO ever. The honest statistical prior for a megacap listing is not doom. It is roughly market performance, with a violent path.

So the drawdown table does not predict that SpaceX falls. It predicts that whoever owns it in year one should expect a moment when it is down a lot, and the relevant question becomes who is holding when that moment arrives. The answer, uniquely in this structure, includes everyone with a Nasdaq-100 tracker, added at day 15, weighted at three times float, without consent. The historical drawdown statistics were generated by IPOs whose passive inclusion came after seasoning. This one front-loads the passive base into the most statistically violent stretch. That is the new variable. It has no historical table.

The Anthropic discrepancy

One contract inside the AI segment deserves its own ledger entry, because the filing and the chief executive describe it differently.

The S-1 discloses a compute agreement under which Anthropic pays $1.25 billion per month for access to the Colossus GPU clusters in Memphis, over 220,000 Nvidia GPUs and more than 300 megawatts of power. Coverage of the filing, including WIRED’s, frames the contract as running through May 2029, roughly $45 billion in total, and reports that Anthropic confirmed the figures. That framing makes the deal the anchor of the AI segment’s revenue story and a load-bearing wall of the $1.75 trillion valuation.

On May 28, Musk publicly described the arrangement as a six-month lease. Both sides hold a 90-day cancellation right.

Both descriptions reference the same contract. They are not the same number. A $45 billion commitment through 2029 and a 180-day arrangement with a quarterly exit are different assets, and the gap between them is most of the AI segment’s claim to durable revenue. The segment lost $2.47 billion in Q1 on roughly $800 million of revenue, which means the Anthropic rate sits below SpaceX’s current cost to operate the cluster. The price reflects strategy, not unit economics. Whichever description of the term is operative, the buyer of SPCX on Friday is underwriting it.

The strongest version of the bull rebuttal should be stated plainly, because it is real: subsequent filings disclosed additional AI infrastructure agreements, including with Google, that bring reported contracted AI revenue to roughly $26 billion annually across the two largest customers, per Barchart’s read of the amended filing. If those contracts hold at term, the AI capex stops looking speculative and starts looking like productive assets. If. The cancellation clauses are where the thesis lives.

What the committee said

The legal and regulatory overhang gets one paragraph, because it is disclosed and priced rather than hidden. The S-1 reserves more than $500 million for litigation, driven in part by lawsuits over non-consensual sexualized images generated by Grok, including, per research by the Center for Countering Digital Hate cited in the complaints, an estimated 23,338 images of minors over an eleven-day stretch. Plaintiffs include three Tennessee minors, the City of Baltimore, and a UK member of parliament. Two countries temporarily banned the product. Buyers of SPCX are buying that docket too. It is in the risk factors, all 38 pages of them, next to the company’s own statement that it has a history of net losses and may not achieve profitability.

None of that stopped the order book. Demand reportedly reached $150 billion, roughly twice the offering, with an unusual 30 percent of the float targeted for retail, against a typical 5 to 10. The deal will price. The stock will trade. The index will do what its rules now say it must.

Which returns us to the one institution that looked at the largest IPO in history and applied its existing standards. S&P’s committee wrote that exceptions should not be granted solely based on market capitalization, and then granted none. In a week when an exchange rewrote its index to receive a single company, the most contrarian act in American finance was a committee doing nothing.

A closing disclosure, since this publication runs on them. I have never paid for Starlink. I used it once, on a Qatar Airways flight from Singapore to New York. No login, no payment screen, fourteen hours of flawless connectivity over two oceans. The product is not the question. The product was never the question. The price of the wrapper around it, and the rules rewritten to deliver that wrapper into your index fund fifteen days after it starts trading, is.

Position disclosure: no position in SPCX, and no intention to initiate one.