Half Of Big Tech’s AI Profit Is Imaginary

Alphabet booked $28.7B in paper gains on Anthropic last quarter. Amazon did the same. The $1.6 trillion AI cloud backlog is mostly two unprofitable startups. This is what the 2001 telecom swaps looked

TLDR:

Three of the most powerful people in AI (Sam Altman, Jensen Huang, and Dario Amodei) walked back the jobs apocalypse narrative in the span of two weeks, right as OpenAI and Anthropic prepare to file for blockbuster IPOs. That timing is not a coincidence. The labor narrative is softening because the underlying financial structure is becoming harder to defend.

Here is what that structure actually looks like. Alphabet booked $28.7 billion in profit last quarter, which was a paper markup on its Anthropic stake, not a customer dollar. Amazon did roughly the same. The combined $1.6 trillion cloud backlog held by the four hyperscalers is concentrated in two AI labs that lose money on every token they sell. Those same labs spend most of their revenue right back on cloud compute rented from the companies that funded them in the first place.

It is a circle. Money goes from hyperscaler to lab, the lab spends it on the hyperscaler’s cloud, and both sides book the same dollars as growth. We have seen this movie before. In 2001 it was called Global Crossing and Qwest, and it ended in bankruptcy and fraud charges. The only difference today is that the AI version is legal.

Here’s the full case.

The tell

In the span of two weeks in late May 2026, three of the most powerful figures in artificial intelligence quietly walked back the story they had been telling for two years.

Sam Altman, speaking at a Commonwealth Bank of Australia conference in Sydney on May 26, said he had been wrong about AI eliminating jobs. His words: “I’m delighted to be wrong about this. I thought there would have been more impact on entry-level white-collar jobs being eliminated by now than has actually happened.” He added that the jobs picture was “likely to be very different from what we thought.”

The same week, Nvidia CEO Jensen Huang called the AI layoff explanation “lazy” and “irresponsible,” asking the obvious question nobody pushing the narrative wanted to hear: “AI has just arrived. How is it possible they’re already losing jobs?” Anthropic’s Dario Amodei, who a year earlier had warned AI could wipe out half of entry-level white-collar jobs, was softening his language in the same window.

Here is the context that makes the timing matter. OpenAI is reportedly preparing a confidential filing for a US IPO in the coming weeks, potentially targeting a $1 trillion valuation and raising at least $60 billion. Anthropic is on a similar track. When the people selling a story start dismantling it right before they cash out, the right question is not whether they had a change of heart. The right question is what they can see on the balance sheet that the public cannot.

The answer is that the revenue underneath the AI boom is not what it appears to be. Some of it is a paper entry. Some of it is the same dollar counted twice. And a dangerous amount of it depends on two companies that have never turned a profit.

The paper-gain machine

Start with the most striking number of the last earnings season.

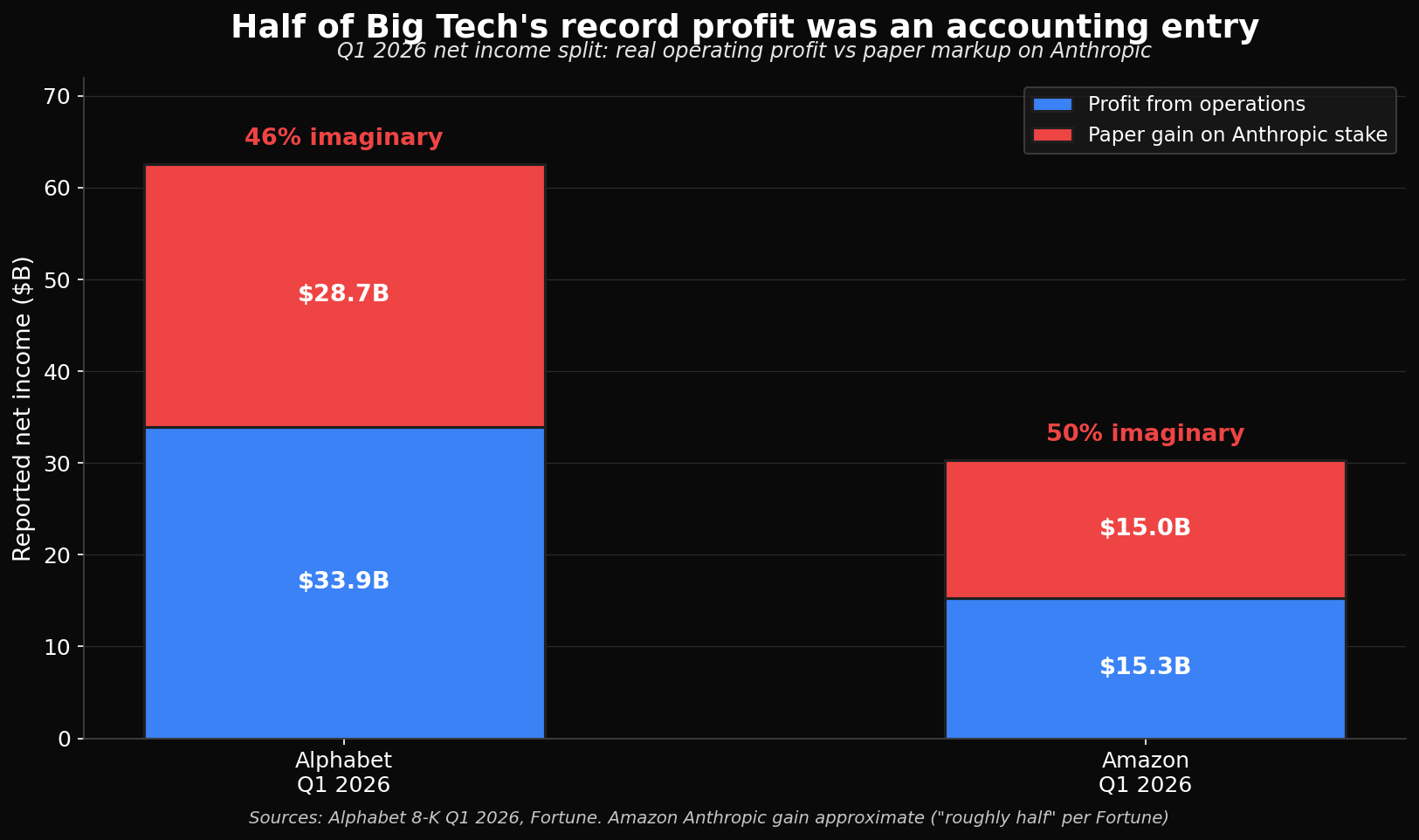

In the first quarter of 2026, Alphabet reported $62.6 billion in net income, up 81% year over year. A blowout quarter by any measure. Except that $28.7 billion of that profit was not a profit in any sense a normal person would recognize. It was a mark-to-market gain on Alphabet’s equity stake in Anthropic.

Here is how that works. When a company holds a stake in a private business and that business raises money at a higher valuation, accounting rules let the stakeholder mark up the value of its holding and book the increase as income. No cash changes hands. No customer pays anything. The startup simply raised a new round at a higher price, and the investor records the unrealized gain as if it were earnings.

Amazon ran the same play in the same quarter. Its net income surged 77% to $30.3 billion, with roughly half of that attributable to the markup on its own Anthropic stake. Two of the largest companies on earth posted record profits, and a very large share of those profits came from marking up the value of a private AI lab that has never made money.

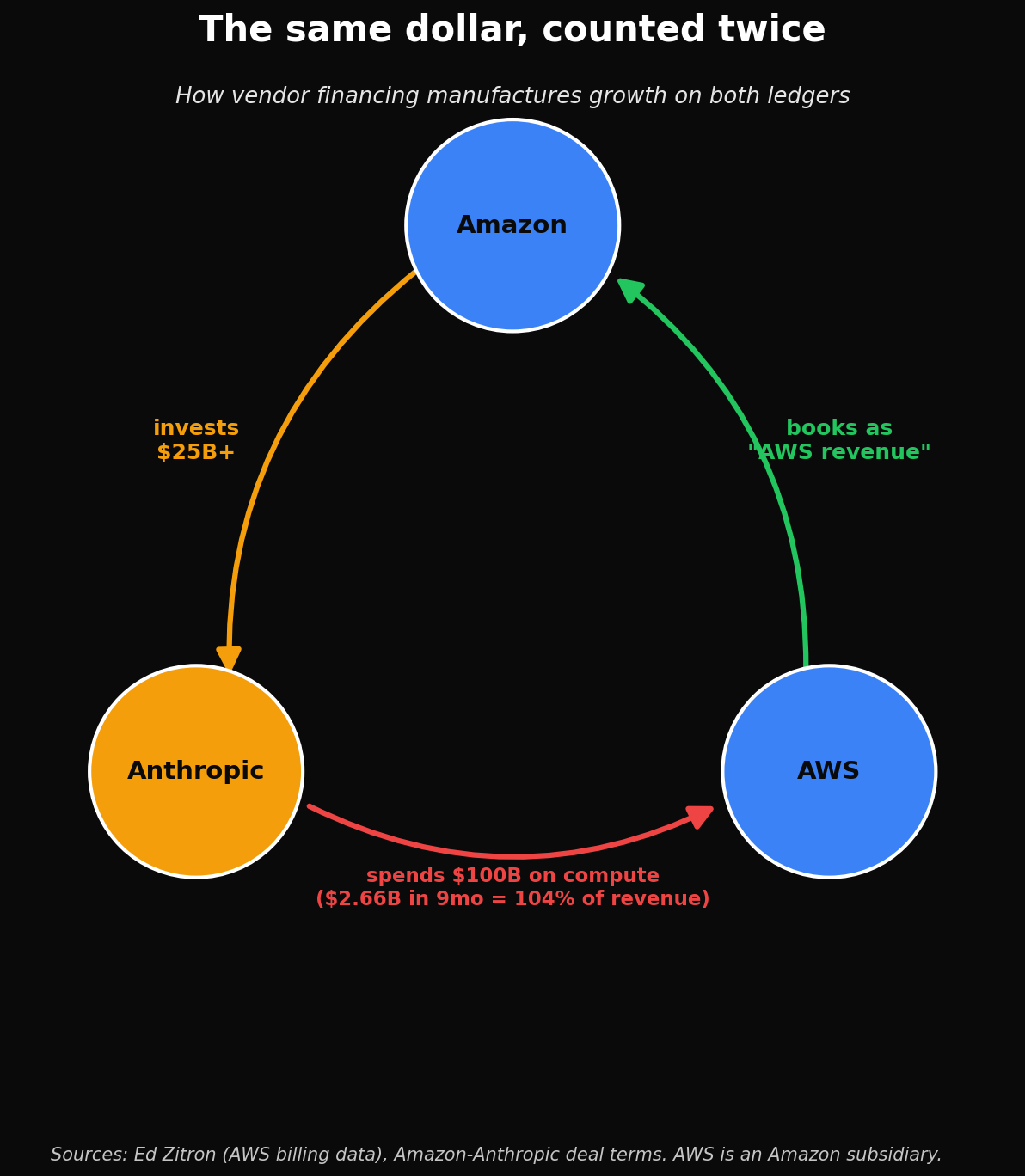

The tax expert Robert Willens put his finger on the strange part. These companies, he noted, are able to influence the value of an asset they own and then mark that asset to market through transactions with the very same entity. Amazon invests in Anthropic, does business with Anthropic, and books gains when Anthropic’s valuation rises. The investor, the customer, and the supplier are arranged in a circle, and the circle generates reported profit.

The mechanism is not theoretical. Anthropic’s Series H funding round closed at a $965 billion post-money valuation. Every step up in that number flows onto the balance sheets of its investors as reported profit, without a single customer dollar changing hands. When the valuation rises, the stakeholders book the gain. When it eventually stops rising, the same mechanism runs in reverse.

This is not illegal. It is not even unusual under current accounting standards. But it means that a meaningful slice of Big Tech’s headline AI-era profitability is an accounting entry tied to private valuations that the same companies help set.

The circle

The paper gains are the visible symptom. The vendor financing loop underneath is the engine.

The clearest documented example involves Amazon and Anthropic. Amazon has invested billions into Anthropic across multiple rounds, taking a stake reported at between 15 and 19 percent. In late 2025 it committed another tranche, and simultaneously Anthropic committed to roughly $100 billion in spending on Amazon Web Services over the following decade. Amazon gives Anthropic money. Anthropic gives the money back to Amazon as cloud spending. Amazon books that spending as AWS revenue.

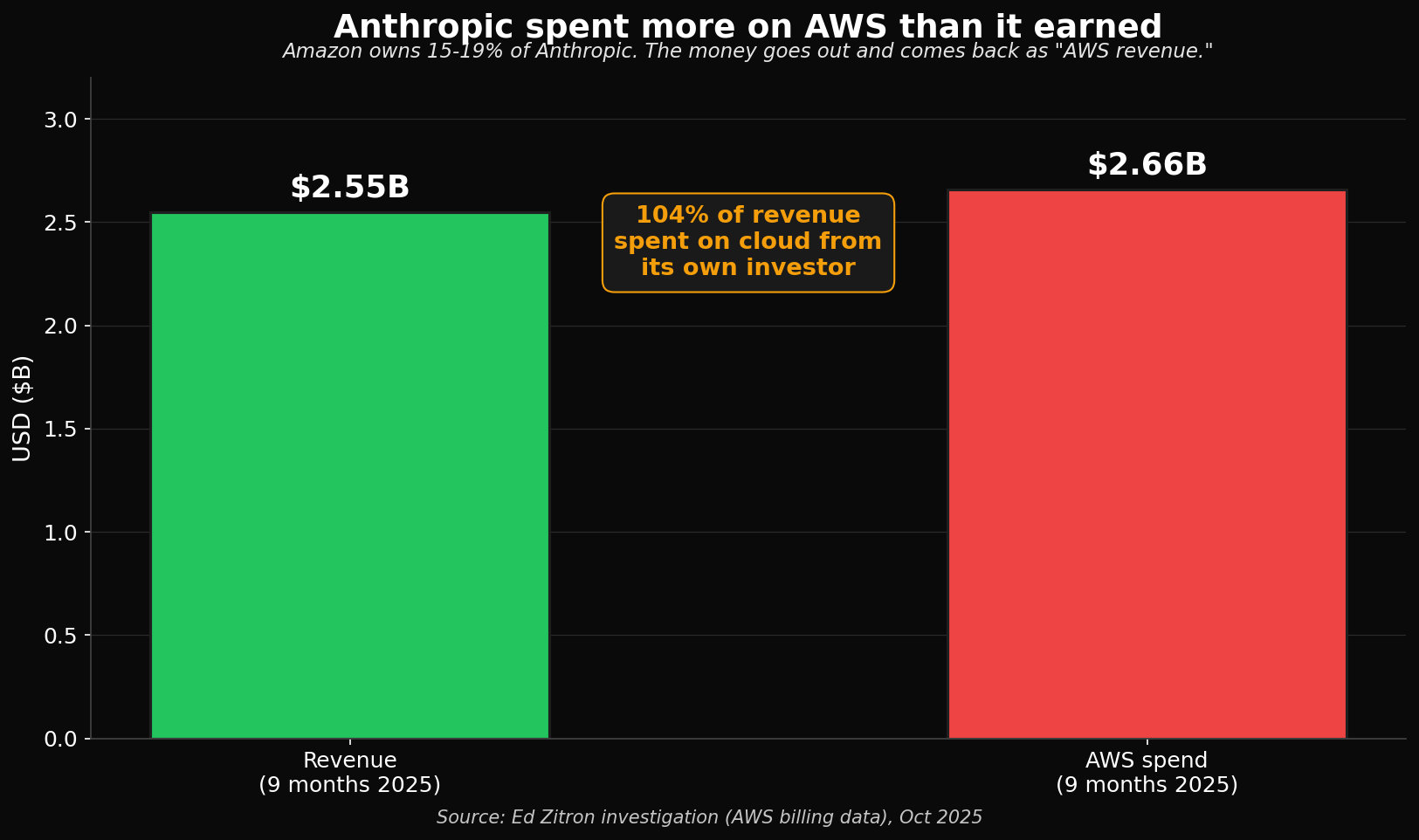

The numbers on the Anthropic side are stark. According to an investigation by Ed Zitron drawing on AWS billing data, Anthropic spent $2.66 billion on Amazon Web Services in the first nine months of 2025 against $2.55 billion in revenue over the same period. That is 104% of revenue going straight back to its largest investor in the form of cloud bills. In January 2025 the ratio was even more extreme, with a reported $185.5 million AWS bill against $72.9 million in revenue, or more than 300%.

The same structure appears across the industry. Microsoft put $13 billion into OpenAI, much of it in the form of Azure cloud credits, which OpenAI then spent running its models on Azure, which Microsoft recorded as cloud revenue. Amazon struck a parallel arrangement with OpenAI. Nvidia invests in the labs that then commit to buying Nvidia chips.

In each case the same dollar is doing double duty. It counts as an investment on one ledger and as revenue on another. The growth story that justifies hundreds of billions in capital expenditure is, in part, a function of money moving in a circle rather than new money entering the system from paying customers

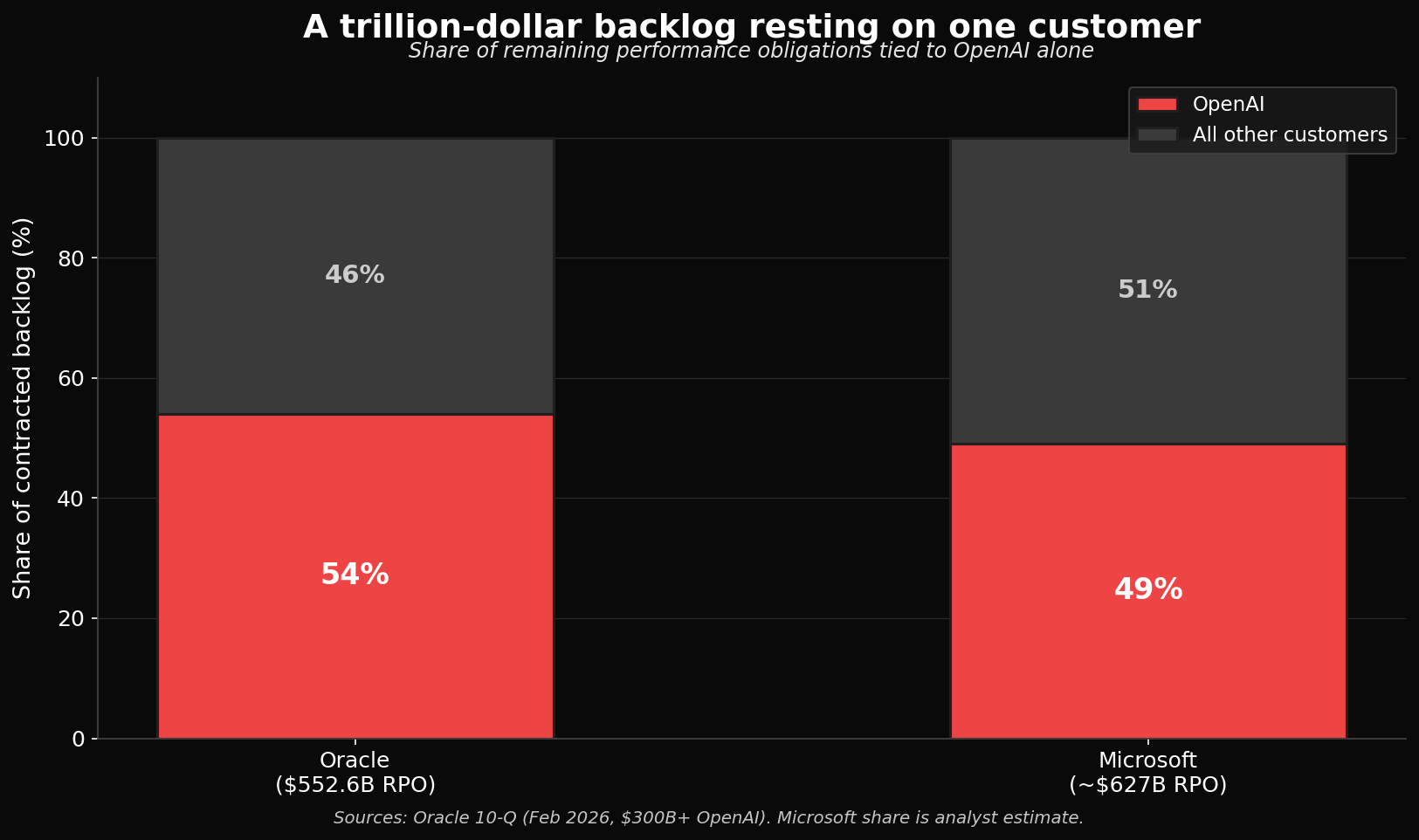

Two customers holding up a trillion-dollar backlog

When hyperscalers report their growth, the headline figure analysts watch is remaining performance obligations, or RPO. It represents contracted future revenue, the backlog of deals already signed. The combined RPO across Microsoft, Oracle, Amazon, and Google now stands at roughly $1.6 trillion. That number is the foundation of the entire AI infrastructure bull case.

Look at what it actually rests on.

Oracle reported $552.6 billion in remaining performance obligations as of the end of February 2026. More than $300 billion of that, roughly 54%, comes from a single customer: OpenAI. Microsoft’s commercial RPO of around $627 billion is, by analyst estimates, close to half tied to OpenAI as well. A backlog that Wall Street treats as evidence of broad, durable demand is, in reality, concentrated in two AI labs that have never been profitable and that fund their compute purchases through capital raises rather than operating cash flow.

The market has started to notice. Oracle raised $18 billion in debt in September 2025 and was reportedly seeking tens of billions more to finance the data center buildout it promised OpenAI. Oracle’s credit default swap spreads, the cost of insuring against an Oracle default, have widened to their highest levels since 2009. Bond investors are pricing in the risk that a backlog dependent on one unprofitable customer might not convert into cash.

The numbers do not work even when you cheat

Here is the part that should end the debate, and it comes from an investment bank, not a short seller.

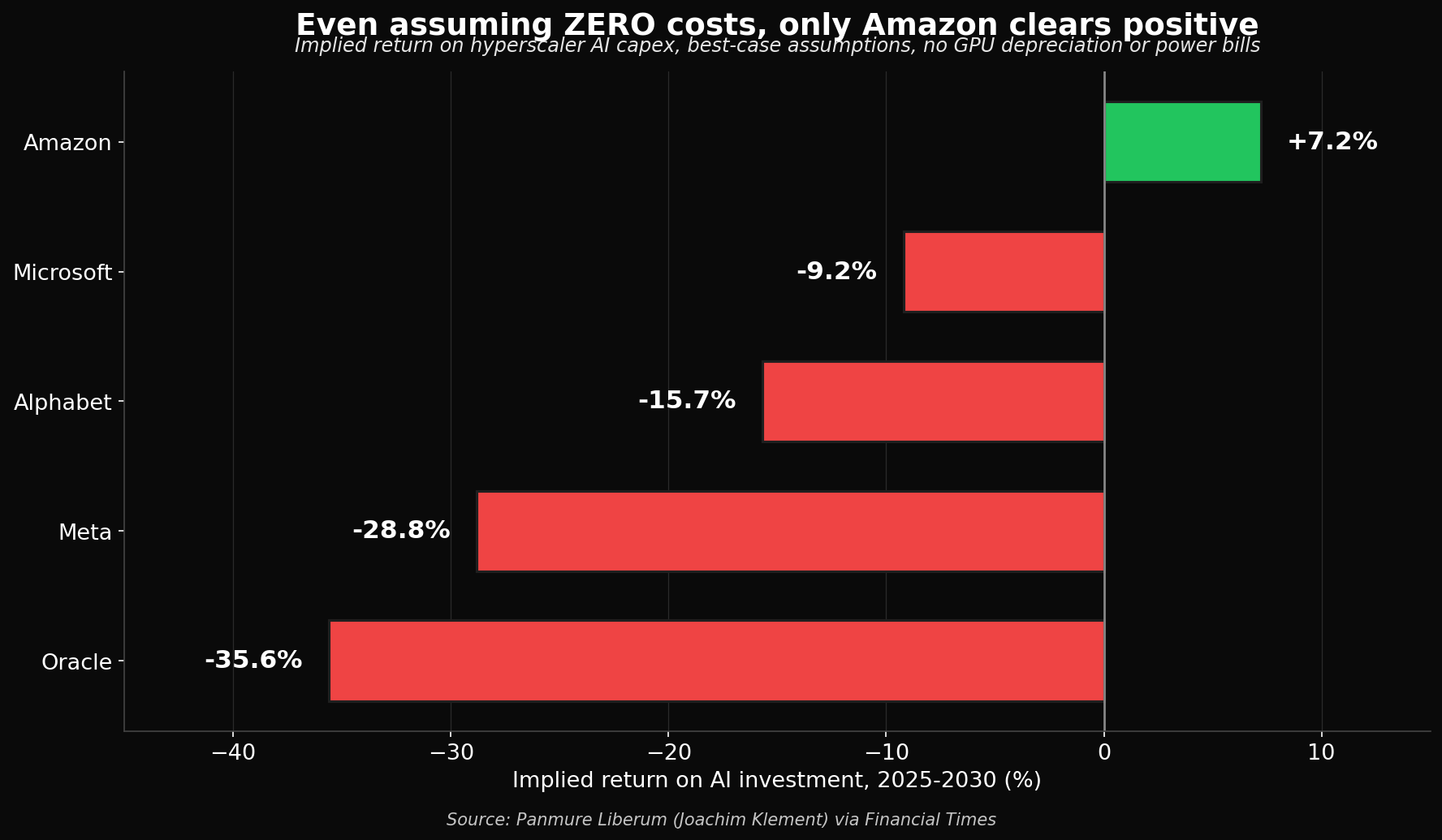

Joachim Klement, a strategist at the brokerage Panmure Liberum, modeled the implied return on the AI capital expenditure of the five largest hyperscalers from 2025 to 2030. He did it under the most generous possible assumptions: zero operating costs, top-end revenue gains, pure projected revenue measured against capital spending. No GPU depreciation, no power bills, no salaries. Just the best case.

Even then, four of the five posts negative implied returns. Microsoft comes in at -9.2%. Alphabet at -15.7%. Meta at -28.8%. Oracle, the most OpenAI-dependent of the group, lands worst at -35.6%. Only Amazon cleared positive, at a slim +7.2%, helped by its custom silicon. And remember, those are the numbers before a single real cost is subtracted. The actual returns are worse.

Klement’s broader math is just as stark. The five hyperscalers would need to find somewhere between $2 trillion and $5 trillion in additional annual revenue to justify their planned data center spending, which is projected to exceed $600 billion in 2026 alone. To get there at current capex-to-sales ratios, they would have to roughly quadruple their revenues. His conclusion, in his own words, is that “if the hyperscalers continue on the current trajectory, the AI boom will become one of the largest destructions of shareholder value in history.” He also calculates that the buildout is already 60% larger than the dotcom bubble, with technology capital expenditure now accounting for nearly all of US GDP growth.

This is not a fringe view from a permabear. It is an investment bank running the arithmetic and finding that the best case loses money.

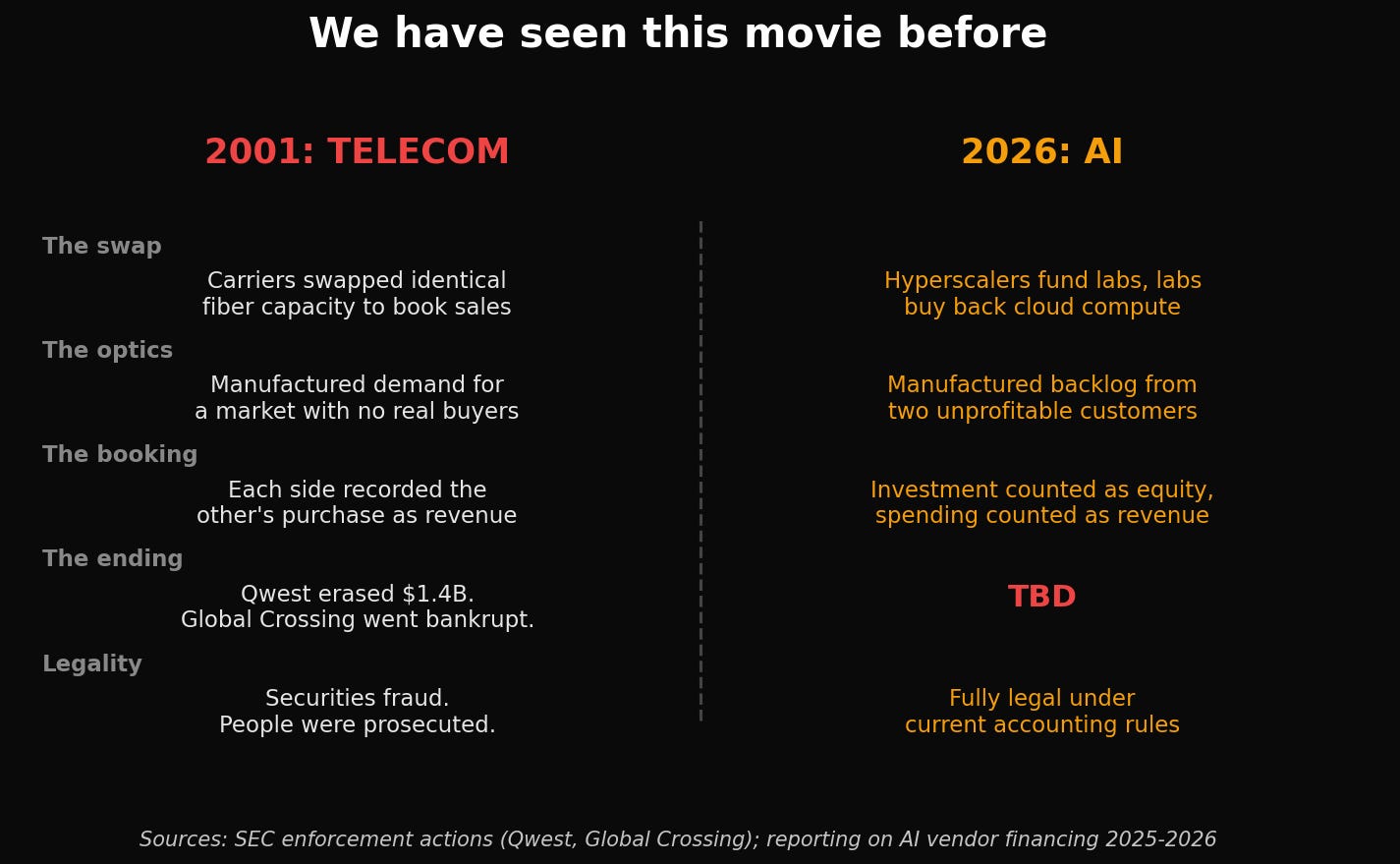

We have seen this before

Strip away the word “AI” and the structure is familiar. It is the telecom bubble of 2001.

In the late 1990s, telecom companies needed to show booming demand for fiber-optic capacity to justify their valuations and their capital spending. Some of them manufactured that demand by swapping capacity with each other. Global Crossing and Qwest Communications famously exchanged essentially identical fiber-optic network capacity, each booking the other’s purchase as revenue. The trades created the appearance of a thriving market, while no real end demand existed underneath.

When the music stopped, Qwest was forced to erase $1.4 billion in improperly recognized income. Global Crossing filed for bankruptcy in early 2002. Executives at both companies faced prosecution. The swaps had been securities fraud.

The AI version is mechanically the same. Capital flows in a circle between a small number of large players, each booking the flow as growth, creating the appearance of demand that outruns the real paying market underneath. The one meaningful difference is that the 2001 swaps were illegal, while the 2026 vendor financing loop is fully permitted under current accounting rules. That should be reassuring and is not. The fraud in 2001 was the deviation from the rules. In 2026, the rules themselves accommodate the circularity.

Where it breaks: the real world

A circular economy of subsidized compute can sustain itself only as long as the money keeps circling. The moment the technology leaves the subsidy loop and meets a real enterprise customer with a hard budget, the unit economics show their true shape. And that is exactly what has started to happen.

Uber rolled out Claude Code to 5,000 engineers in December 2025. By April 2026, the company had exhausted its entire annual AI budget, four months into the year, against a $3.4 billion R&D base. Heavy users were costing up to $2,000 per person per month. The CTO’s line was telling: “I’m back to the drawing board, because the budget I thought I would need is blown away already.”

The admission then climbed the org chart. In late May, Uber’s president and COO Andrew Macdonald described the moment he learned the company had blown its annual AI budget in four months as “head-exploding.” His assessment of the spend was blunt: “If you’re not actually able to draw a direct line to how many useful features and functionality you’re shipping to your users, that trade becomes harder to justify.” When the COO of a company where 95% of engineers use AI monthly and 70% of committed code is AI-generated cannot draw a line from the spend to the product, the ROI is not lagging. It is missing.

Then came the data point that should worry every CFO in tech. In May 2026, Microsoft began canceling thousands of internal Claude Code licenses across its Experiences and Devices division, covering Windows, Microsoft 365, Outlook, Teams, and Surface, with a June 30 deadline. The official reason was tool consolidation. The real one was the cost. The company that put $13 billion into OpenAI, which runs the Azure infrastructure powering much of the model layer, that has effectively unlimited cloud capacity, looked at the bill for a competitor’s coding tool and decided it was not worth paying. If Microsoft cannot justify the cost, the question of who can becomes very short.

The pattern is now widespread enough that Axios called it “Corporate America’s AI reckoning.” In that reporting, an AI consultant said one of their clients spent half a billion dollars in a single month after forgetting to set usage limits on Claude licenses for employees. The CEO of CloudBees offered the darkest interpretation of the layoff wave: workforce cuts, he suggested, may simply be “the only lever they can pull” to offset their AI bills. Read that against my last piece. The layoffs were never really about AI replacing workers. They were partly about paying for the AI. One CTO told Axios that employees were using frontier models to check the weather, which gets expensive fast when enterprise plans are not actually all-you-can-eat.

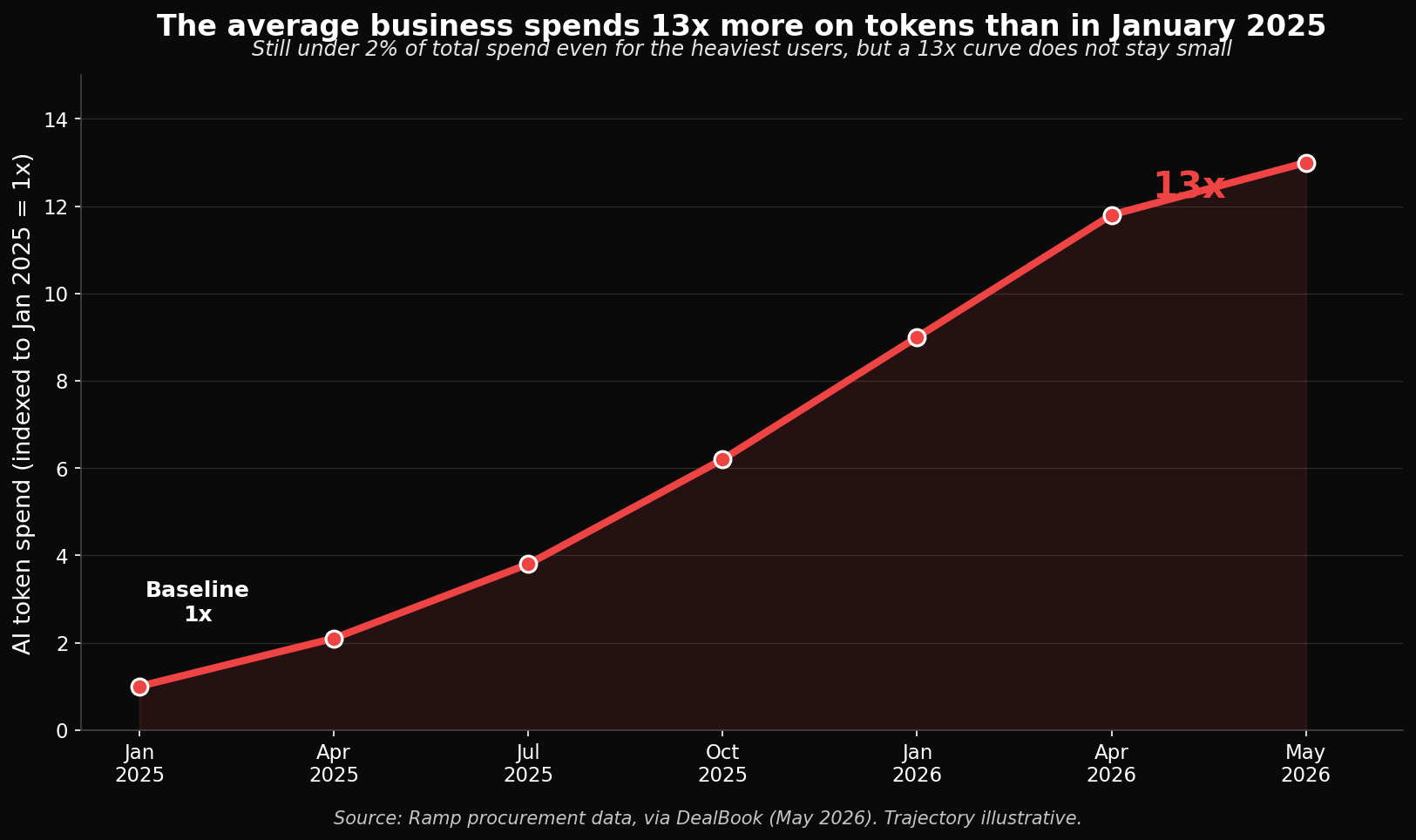

The broader spend data confirms the trajectory. Procurement firm Ramp reports that the average business now spends roughly 13 times more on AI tokens than it did in January 2025. Tokens remain under 2% of total spend even for the heaviest users, but a 13x annual growth rate does not stay small for long. GitHub, owned by Microsoft and running on Azure, is abandoning flat-rate pricing for Copilot in June 2026 precisely because the flat-rate model was bleeding money on heavy agentic users. And Nvidia’s own Bryan Catanzaro admitted in April that “the cost of compute is far beyond the costs of the employees,” which is the GPU maker conceding that the thing meant to replace expensive humans currently costs more than the humans.

The pitch was that tokens would get cheaper and agents would replace workers. Outside the subsidy loop, tokens are expensive and getting more so on a per-workload basis, and the labs are quietly walking back the replacement story.

The best argument against all of this

The strongest counter to this thesis is not a denial of the numbers. It is the Solow Paradox.

In 1987, the economist Robert Solow quipped that “you can see the computer age everywhere but in the productivity statistics.” Massive corporate IT investment through the 1970s and 1980s had failed to show up in measured productivity. Then, beginning around 1996, the productivity payoff from computing and the internet finally arrived, years after the capital had been spent. The lag was real, and betting against the technology during the lag would have been a mistake.

In May 2026, the Federal Reserve Bank of San Francisco argued that AI may be on the same curve. Labor productivity is rising even as total factor productivity stays flat, exactly the divergence seen in the mid-1990s before the internet’s gains materialized in the aggregate data. Maybe, the argument goes, the AI ROI is real and simply lagging, and the capital expenditure will be vindicated in a few years.

It is a serious argument, and it deserves a serious answer. Here is mine. The 1990s internet buildout was funded by real demand and real customer cash, not by a circle of hyperscalers marking up their own investments and booking each other’s spending as revenue. The Solow lag explains why productivity gains might show up late. It says nothing about whether reported revenue is circular or whether reported profit is a paper markup. Those are accounting questions, not timing questions. The Atlanta Fed found that executives perceive larger AI productivity gains than researchers can actually measure in company revenue, attributing the gap to “delayed output realizations.” Maybe. Or maybe it is the same wishful thinking that led 75% of executives in a separate survey to admit their AI strategy was “more for show” than real guidance. The lag may well be real. But a lag in productivity does not turn a circular dollar into a customer dollar.

Why nobody is pricing it in

If the structure is this visible in public filings, why has the market not corrected?

Because the loop is self-reinforcing on the way up. Paper gains inflate reported profits. Inflated profits push up market capitalizations. Higher market caps mean index funds and passive retirement accounts, which buy in proportion to market weight, mechanically purchase more of the inflated stocks. That buying pushes prices higher still. At no point in this cycle does anyone need to verify that the AI revenue has been converted into actual cash profit. The machine runs on reported figures, and the reported figures are partly manufactured by the circularity.

The most mispriced risk in global finance right now is not a single company or a single number. It is the widening gap between the optimism on earnings calls and the invoices landing on corporate desks. One side is a story. The other side is a budget. They cannot both be right indefinitely.

What breaks first

A few leading indicators are worth watching because they will move before the headline numbers do.

Oracle’s credit spreads are the clearest early warning, already at their widest since 2009. If they keep widening, the bond market is telling you it does not believe the OpenAI backlog converts to cash. Watch for more hyperscalers quietly canceling AI tools internally, the way Microsoft did, because internal cancellation is the most honest signal a company can send about unit economics. Watch the IPO pricing for OpenAI and Anthropic, because the bankers setting those prices have seen the real numbers and the valuations they land on will reveal what the smart money actually believes. And watch whether the labs hit their internal revenue targets, because the entire backlog assumes they grow into commitments that currently exceed their revenue many times over.

When the markup machine slows, the sequence is predictable. Capital expenditure slows. The labs miss revenue targets. The paper gains reverse into paper losses. And the circular flow that looked like growth on the way up looks like contagion on the way down.

Disclosure: I work at Adobe as a solution consultant. This piece is about the financial structure of the foundation layer, the labs, and the hyperscalers building the AI infrastructure. It is not about application-layer software serving real customers who pay real money for real outcomes, which operates on entirely different unit economics. The bubble I am describing is in the foundation, not in the products built on top of it.

The connection

My last piece argued that the AI layoff narrative was breaking and that a selective rehire wave had already begun. This is the other half of that story. The labor market repricing was the symptom. The capital market mirage is the cause.

When the loop unwinds, the layoffs reverse, but the rehire is selective, exactly as the labor data already shows. The companies that survive the correction will hire the people who can actually wield these tools productively, and they will let everyone else compete for a shrinking pool of unautomated work. The capital story and the labor story are the same story told at two different layers of the stack.

The technology is real. The productivity gains may even be real, eventually. But a real technology can sit on top of a fake balance sheet for a surprisingly long time, right up until it cannot.

In 2000, the internet was real, too. Cisco was the company selling the picks and shovels for it, the most valuable company in the world at its peak. The internet went on to remake the entire economy, exactly as promised. Cisco’s stock took twenty-six years to climb back to where it traded in March 2000. Being right about the technology and being right about the returns are two completely different bets.

Where do you sit when the correction comes? I built ismyjobscrewed.com to help you find out, and to map the upskilling path that puts you in the cohort that gets hired rather than the one that gets cut.

Mispriced covers tech at the intersection of AI, data, and crypto. Following the capex, finding what the market got wrong. Subscribe for the next one.

Sources and full reference list: https://telegra.ph/Half-Of-Big-Techs-AI-Profit-Is-Imaginary-References-05-30