Ethereum Already Won. Your ETH Didn't.

ETH is 9.77% of the market cap, down 57% from its high, while JPMorgan builds on Base and routes the token nothing. The network and the asset came unwelded, and almost everyone is pricing incorrectly.

In May 2026, Ethereum did more than it has ever done. 64% of crypto’s transactions, half of all stablecoins, $628 billion settled in a single month. And ETH the token, a $244 billion asset trading near $2,025, earned almost nothing for it. Base fees collapsed after the Dencun upgrade, the blob fix shipped in December and changed nothing, and the network now burns about 70 ETH a day against 2,820 issued. ETH is inflating. The “ultrasound money” thesis is dead, and even the $250,000 bull deck quietly admits the issuance.

This is not an anti-Ethereum piece, and I hold ETH. Ethereum the network is winning, decisively, on every axis that matters for the next decade. The problem is that everything that makes it win is engineered to give value away, and the market has spent two years pricing the token as if the network were dying. The truth is stranger than that.

The seven loudest voices on ETH are all fighting about one question: whether the token captures the network through fees. They run the full range, from David Hoffman, who just sold every coin he owned, to Standard Chartered, which is calling for $40,000. That argument can be laid to rest. It doesn't.

ETH is not a fee asset and never really was. It is the reserve collateral of the most neutral settlement network on Earth, and you price that the way you price gold: on demand to hold it, not on the toll it collects.

The repricing is not $250,000, and it is not zero. It is a slow migration of monetary and collateral demand toward the asset the whole system is denominated in, plus a free option on institutions, AI agents, and tokenization, eventually routing value through it. It can stay mispriced for years. It has. Here’s the full case.

---

The Week Two Smart People Looked At The Same Chart And Saw Opposite Things

In the last week of May, David Hoffman sold all of his ETH.

This matters because Hoffman is not a tourist. He built Bankless, a media empire, and a decade of his identity on Ethereum. So when he writes that the “ETH is Money” thesis played out rather than failed, that the token got the price it deserves and won’t be rerated up or down, the people who bought ETH because of him listen. His verdict was generous and brutal at once: massively bullish on Ethereum the network, finished with ETH the asset. Ethereum, he wrote, is a giver, not a taker.

The same week, Standard Chartered’s Geoffrey Kendrick told clients that ETH would reach $4,000 this year and $40,000 by 2030. His comparison was Amazon during the dot-com crash, the stock that fell to six dollars while the business got better every quarter.

And here is the most amusing detail. JPMorgan, in the same month, did both at once. On May 19, its research desk told clients ETH was unlikely to reverse years of underperformance against Bitcoin without real improvement in network activity and use, and that upcoming upgrades might not fix it. Then JPMorgan put its own product, a tokenized deposit token called JPMD, live on Base, an Ethereum layer-2. Bullish the network. Skeptical of the token. One institution, living the entire contradiction in a single month.

That contradiction is the whole story. And the data resolves it cleanly, just not in either camp’s favor.

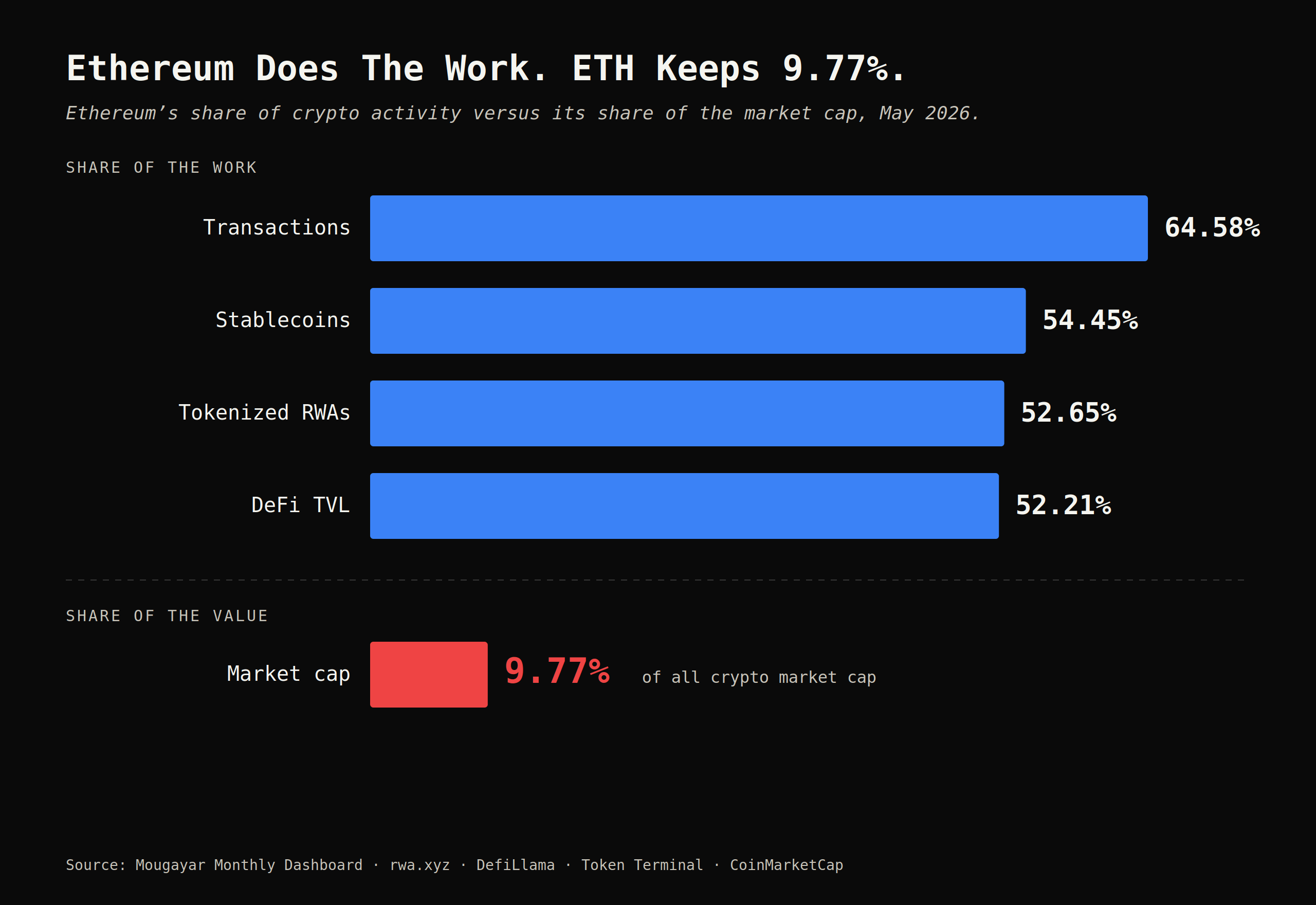

[Ethereum’s share of crypto activity vs share of market cap. Bars at 64% transactions, 54% stablecoins, 53% tokenized assets, 52% DeFi TVL, all in white. Market cap share alone at 9.77% in red, far below the pack. Caption: “Ethereum does the work. ETH doesn’t capture the value.” Source: Mougayar monthly dashboard / rwa.xyz / DefiLlama / CoinMarketCap.]

The Burn Is Dead, And The Bulls’ Own Math Admits It

Start with the number that ends the loudest bull argument.

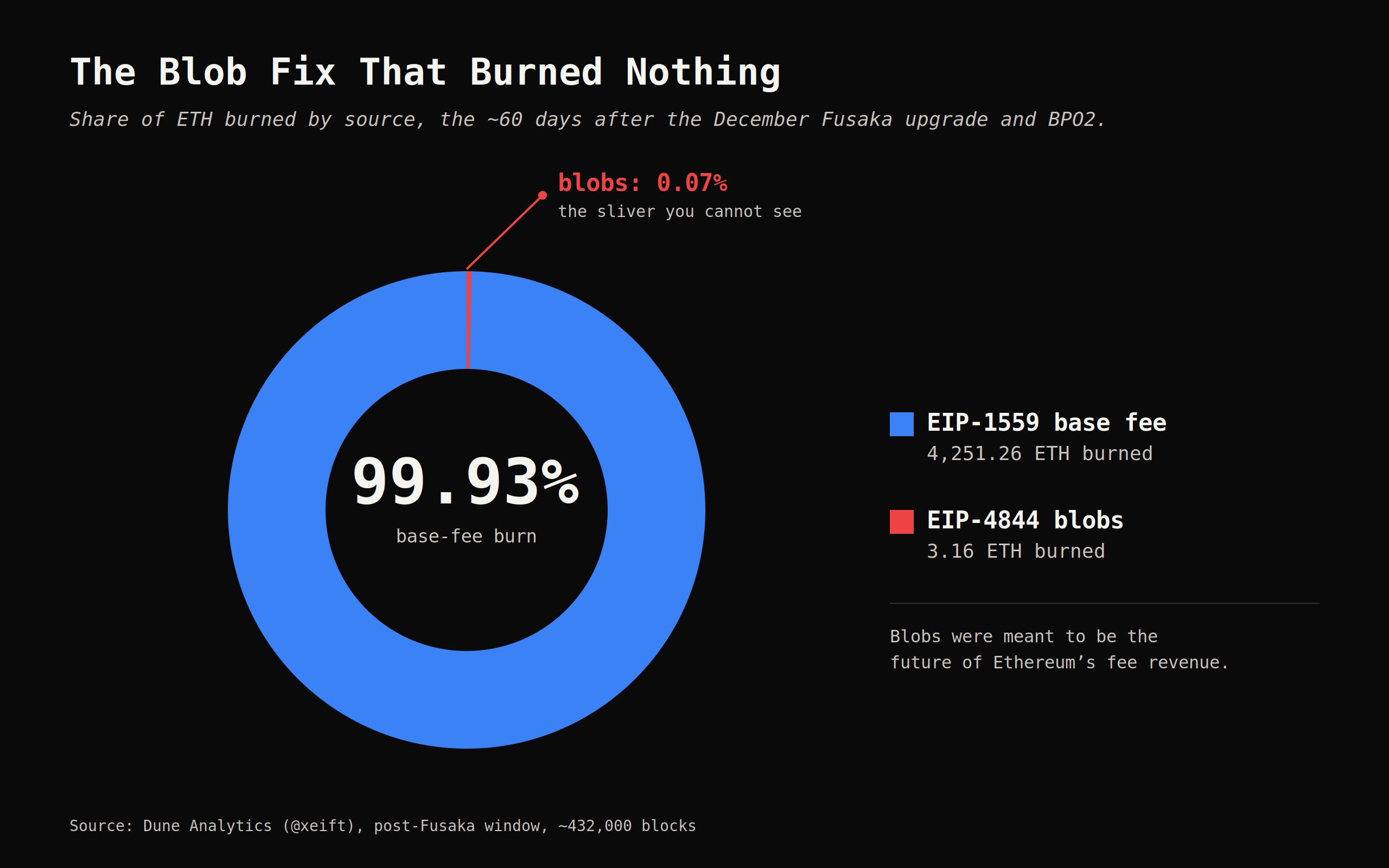

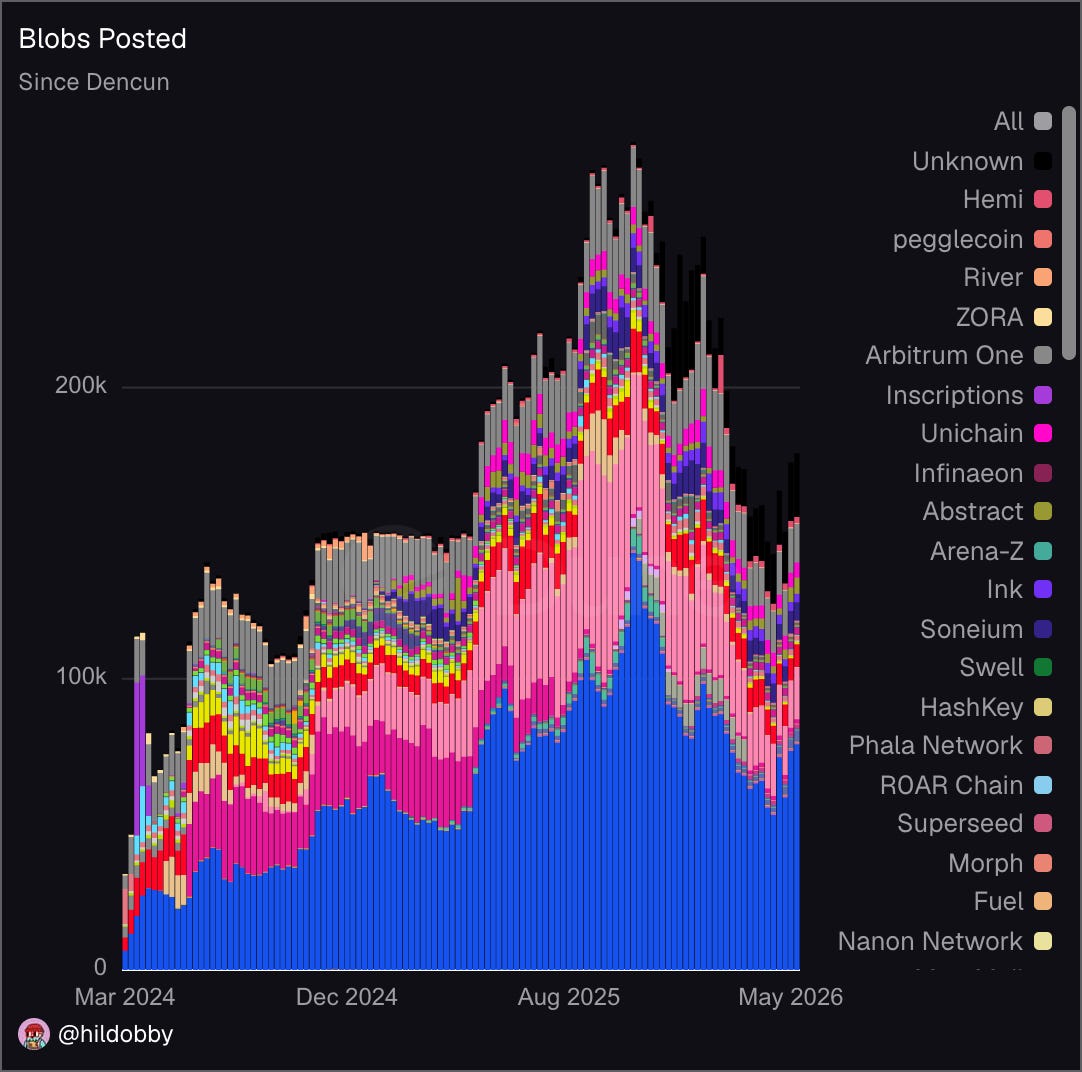

Every bull case eventually rests on the burn: usage rises, ETH gets destroyed, supply shrinks, price climbs. So look at what actually burns. Over roughly sixty days after December’s Fusaka upgrade, Ethereum burned 4,251 ETH through ordinary base fees and 3.16 ETH through blobs, the layer-2 data mechanism that was supposed to be the future of the network’s revenue. Blobs are seven hundredths of one percent of the burn. That is not a rounding error you grow out of. That is the mechanism not existing.

Zoom out, and it gets worse. The network issues about 2,820 ETH a day to validators and burns about 70. ETH is inflating at roughly 0.83% a year. Not ultrasound, not deflationary. Inflationary, today, at an all-time high usage.

The remarkable part is that the bulls know this. Etherealize, the firm behind the $250,000 target, states on its own website that ETH supply has been “flat-to-deflationary since the Merge.” Its own report, three pages from that line, concedes net issuance “has hovered around 0.8%.” The chain says 0.83% inflation. Three numbers, one of them contradicting itself inside one firm’s own materials. When the people calling for $250,000 cannot keep their scarcity story straight across two documents, the scarcity story is over.

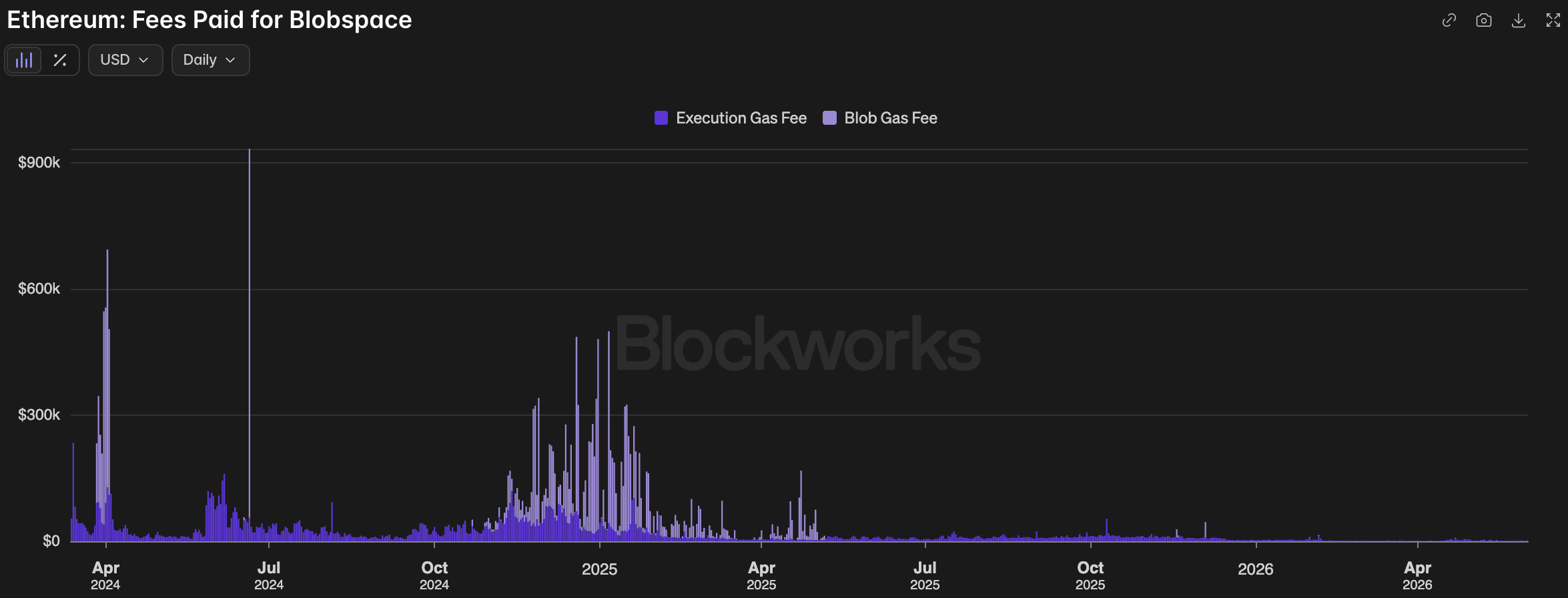

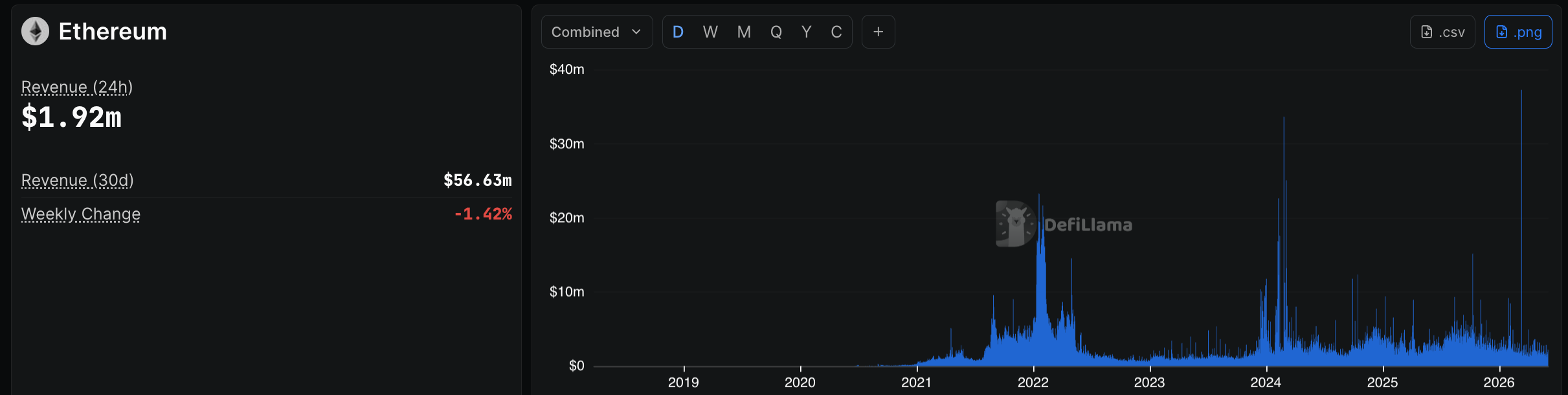

Didn’t December’s upgrade fix this? Fusaka shipped a floor under blob fees so they could never collapse to zero again. It worked. Blob burn rose something like eightfold. But eight times almost nothing is almost nothing, and Ethereum’s monthly revenue chart tells the truth: a peak above $1.5 billion a month in 2021, and a flat line scraping the bottom through 2025 and into 2026.

[Blob burn donut: 99.9% EIP-1559 base fee / 0.1% EIP-4844 blobs, over ~60 days post-Fusaka. Source: Dune (@xeift).]

[Ethereum monthly chain revenue, 2021 to 2026, showing the $1.5B+ peak collapsing to a flat line. ETH-denominated and USD both noted. Source: DefiLlama.]

This Is Not A Bug. It Is The Architecture Working As Designed.

Hoffman’s deepest point is that none of this is an accident.

Ethereum chose the rollup-centric roadmap on purpose. Layer-2 networks do the cheap, fast transactions and pay Ethereum a thin slice for security. How thin? Base, Coinbase’s layer-2, earned more than $94 million in profit and paid Ethereum about $4.9 million for the privilege. Across 2025, every layer-2 combined paid Ethereum roughly $10 million for security, under a tenth of what they kept. The value moved up to the rollups and out to the apps, exactly as the design intended.

And the revenue that does reach the base layer increasingly skips ETH holders entirely. Break down what’s left, as the analyst The DeFi Report does on-chain, and the surviving income is mostly priority fees and MEV tips, which flow to validators. The base fee, the only part that gets burned and the only part that reaches every holder through scarcity, is the shrinking slice of a shrinking pie.

However, this is not an Ethereum disease. Solana, the chain the bears hold up as the winner, runs about $10 million a day in ecosystem fees and routes under 10% to the protocol. SOL inflates around 4%. It has no burn at all. Every general-purpose smart-contract chain gives its value to apps and validators and hands the token holder a thinning toll. The value that the entire sector fights about is mostly absent everywhere. The bears who sold ETH for SOL traded one version of the problem for a worse one.

And the last hope, that blob demand grows until fees finally spike, has the arrow pointing backwards. Blob demand peaked in mid-2025 and has fallen since, even as Ethereum raised the blob target. Rising capacity, falling use. The market is emptying, not filling.

The Institutions Came. They Came To The Layer Above ETH.

The bull story says Wall Street is coming and ETH rides the wave. Wall Street is coming. Watch where it actually lands.

JPMorgan’s JPMD, a tokenized claim on real bank deposits, went live not on Ethereum but on Base, the layer-2. It is the first time a major commercial bank put a deposit product on a public blockchain, and the fees accrue to JPMorgan, to Base, and to Coinbase. Ethereum the base layer earns the same near-zero blob fee as everyone else. The bank validated the ecosystem and routed the token nothing. It is Hoffman’s thesis with a Fortune 50 logo stamped on it.

The same pattern runs through stablecoins, the asset Ethereum supposedly owns. Ethereum holds roughly $163 billion of them, about 54% of global supply, per rwa.xyz. But PayPal’s PYUSD now does more transaction volume on Solana than on Ethereum, and has since the middle of 2025. Ethereum holds the balances. The activity rotates elsewhere.

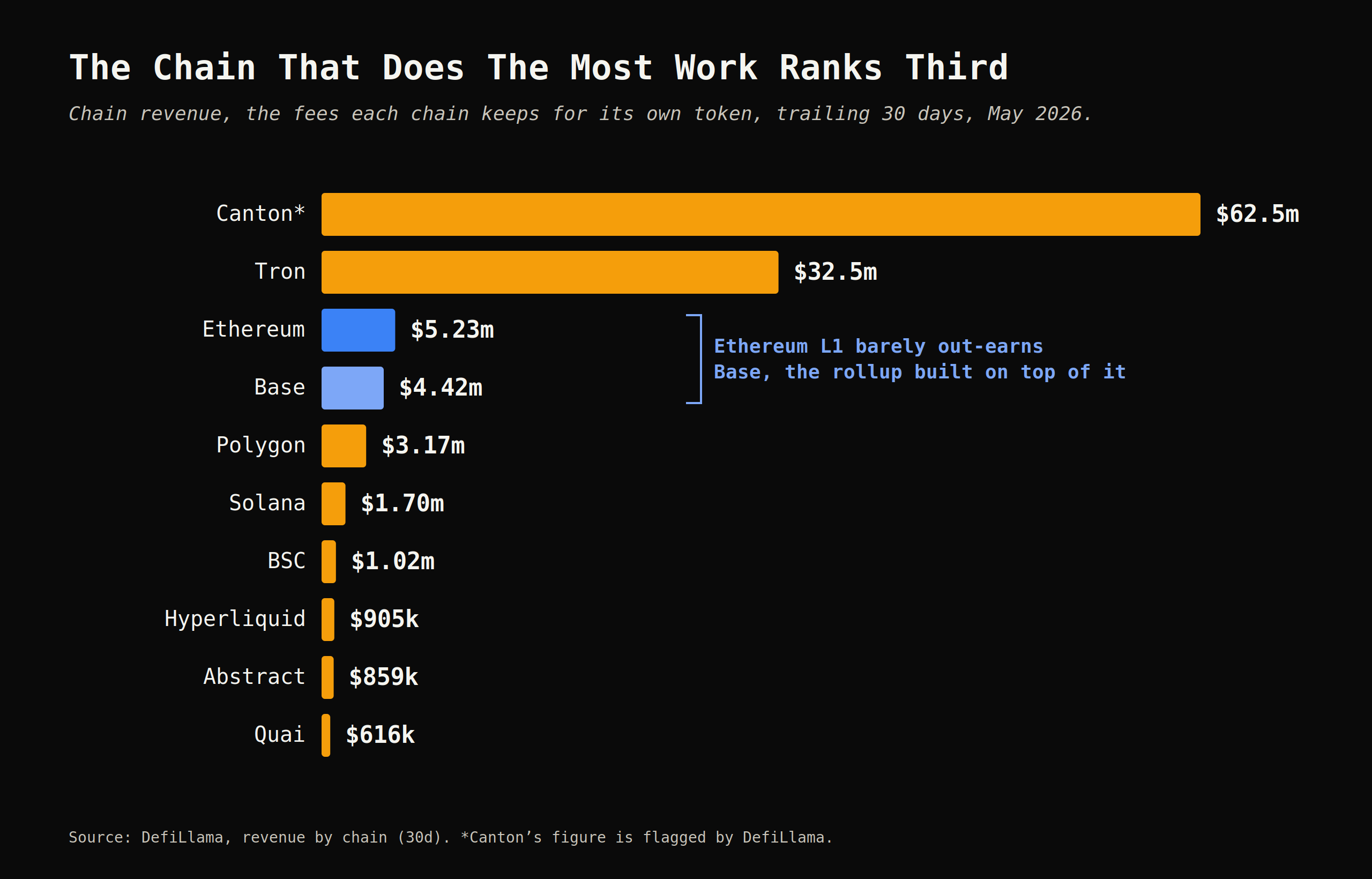

Eighteen months ago, Ethereum’s fee dominance looked permanent. By total fees, the gross amount users pay, Solana, Tron, and Ethereum ran neck and neck in February, around $27, $24, and $23 million for the month. But fees are the top line. What matters for the token is revenue, the slice each chain keeps, and Ethereum is worse than at parity. Over the last thirty days, it kept about $5.2 million, a sixth of Tron's $32 million. And here is the line that should end the argument: Ethereum barely out-earned Base, its own layer-2, which kept $4.4 million. The parent and its own child, nearly tied, both a rounding error next to the volume Ethereum settles. The crown is gone, and the toll barely reaches the token.

But look closer at William Mougayar’s monthly dashboard, where every line traces to a primary source, and a pattern appears that both camps miss. Ethereum’s share is highest exactly where institutions live: 64% of transactions, 54% of stablecoins, 53% of tokenized assets. It is lowest where retail speculates: 26% of NFT volume, 21% of DEX volume. Ethereum is quietly becoming the settlement and collateral layer for serious money. That is the signal the bears overlook and the bulls misprice.

[Stablecoin supply by chain: Ethereum ~$163B / Tron ~$87B / Solana / BSC, with Ethereum’s share line flat-to-eroding over the year. Source: DefiLlama / rwa.xyz.]

The Strongest Bull Case Ever Written, And Why It Breaks Itself

If you want the bull case at full strength, read Etherealize’s “Ethereum and the Era of Productive Money.” It is the most sophisticated argument for ETH in existence, which is exactly why it deserves to be met head-on rather than waved away.

One disclosure first, because it matters: Etherealize describes itself as a product, business-development, and marketing arm for the Ethereum ecosystem, and it represents Ethereum in Washington. This is a registered advocate publishing a $250,000 target for the asset it exists to promote. That does not make it wrong. It makes it the most polished piece of bull marketing the cycle has produced, and we should treat it that way.

The case runs like this. Warren Buffett dismissed gold because it just sits there: own an ounce for eternity, and you still have an ounce. Bitcoin has the same flaw. ETH does not, because you stake it and earn a yield generated by the protocol itself, with no borrower and no counterparty. So ETH becomes the first money in history that compounds in your own hands. Add the rest of the monetary checklist, and if ETH captures even a slice of the roughly $30 trillion premium sitting in gold and Bitcoin, the arithmetic spits out $250,000 a coin.

It is genuinely elegant. It breaks on two facts.

First, the productivity is mostly dilution. We already saw that staking yield comes overwhelmingly from new issuance, not from fees, because the fees collapsed. Paying stakers with freshly printed ETH while everyone else holds still is not a dividend funded by profit. It is the printer moving coins from one pocket to another. “You will own more ETH” is true and nearly empty, because every other holder’s pile inflated right alongside yours. Real productivity is fees, and the fees are gone.

Second, and this is the heart of the whole debate: a monetary premium is the price the market pays for an asset to be boring.

Gold and Bitcoin earn their premium by being inert. Fixed supply, no governance, no surprises, nothing ever changes. That stillness is the entire product. Now look at what Etherealize celebrates about ETH: a quantum-resistance overhaul, a privacy roadmap, zkEVMs, a gas limit tripling, and a hard fork every six months. For a technology platform, that velocity is a triumph. For a monetary premium, it is a disqualification, because money is trusted precisely for what it refuses to do. Etherealize even concedes that ETH is weakest on established history, and then asks you to value it as established money.

You cannot be the most dynamic computer in the world and the most trusted dead asset in the world at the same time. Those are two different products, sold to two different buyers, for opposite reasons. Every bull conflates them. Hoffman, staring at the same chain, simply believes the platform and gives up on the premium. They are each half right, and the half they share is the wrong half.

There is a sharper version of this, and quantum computing just made it concrete. When the cryptographic ground itself can crack, inertness stops being a virtue and becomes a liability. The same refusal to change that makes Bitcoin trustworthy as money is exactly why it is paralyzed on the quantum threat, while Ethereum’s relentless dynamism, the thing that disqualifies it from a pure monetary premium, is what lets it adapt and survive. In a world where the substrate shifts, the adaptive chain is the one that stays money at all. More on that below.

What’s Actually Mispriced, And It Isn’t On Anyone’s Chart

So if it isn’t fees, and it isn’t a $250,000 monetary premium, what is the trade?

Follow the capex. Two things are tightening that have nothing to do with the burn.

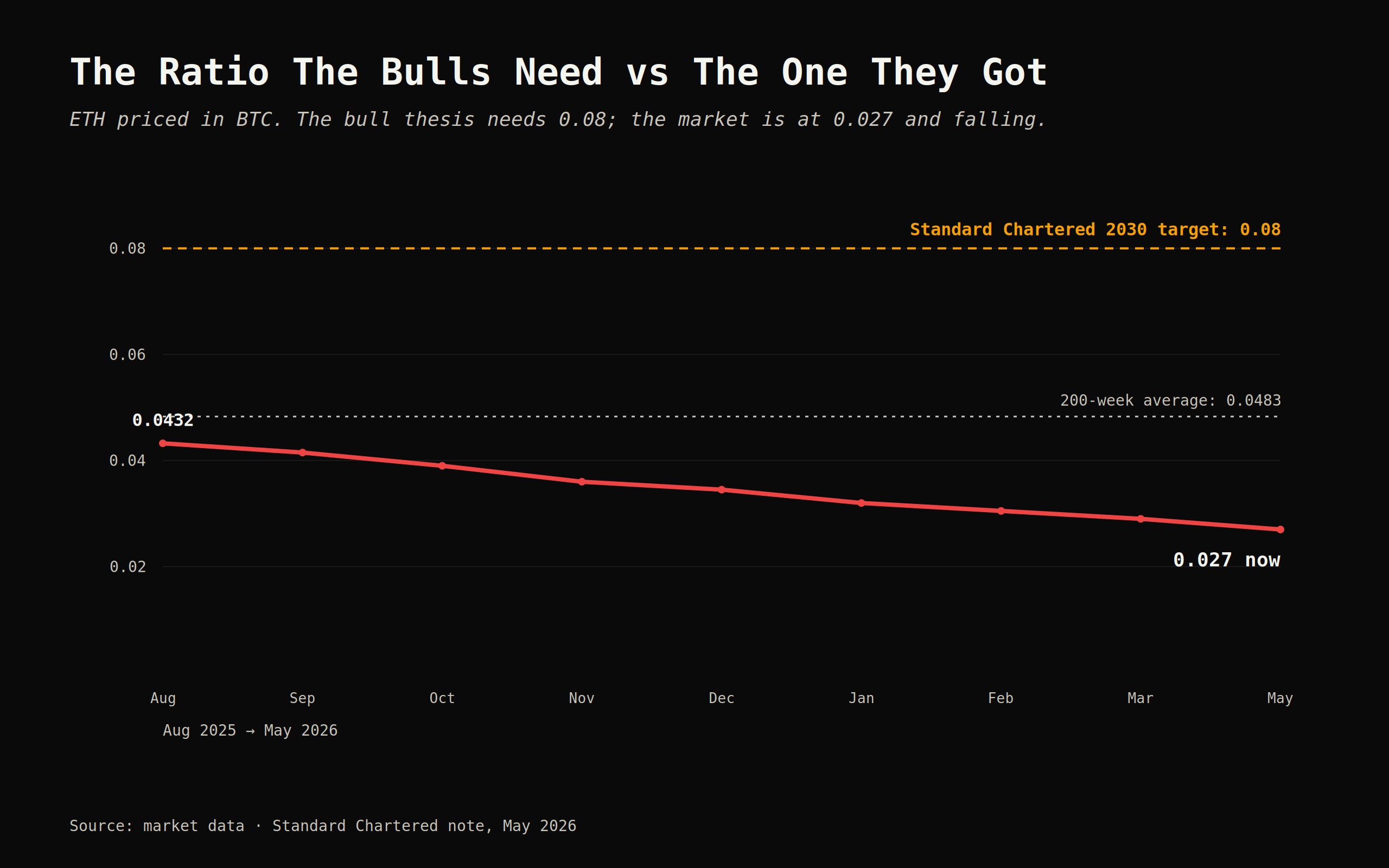

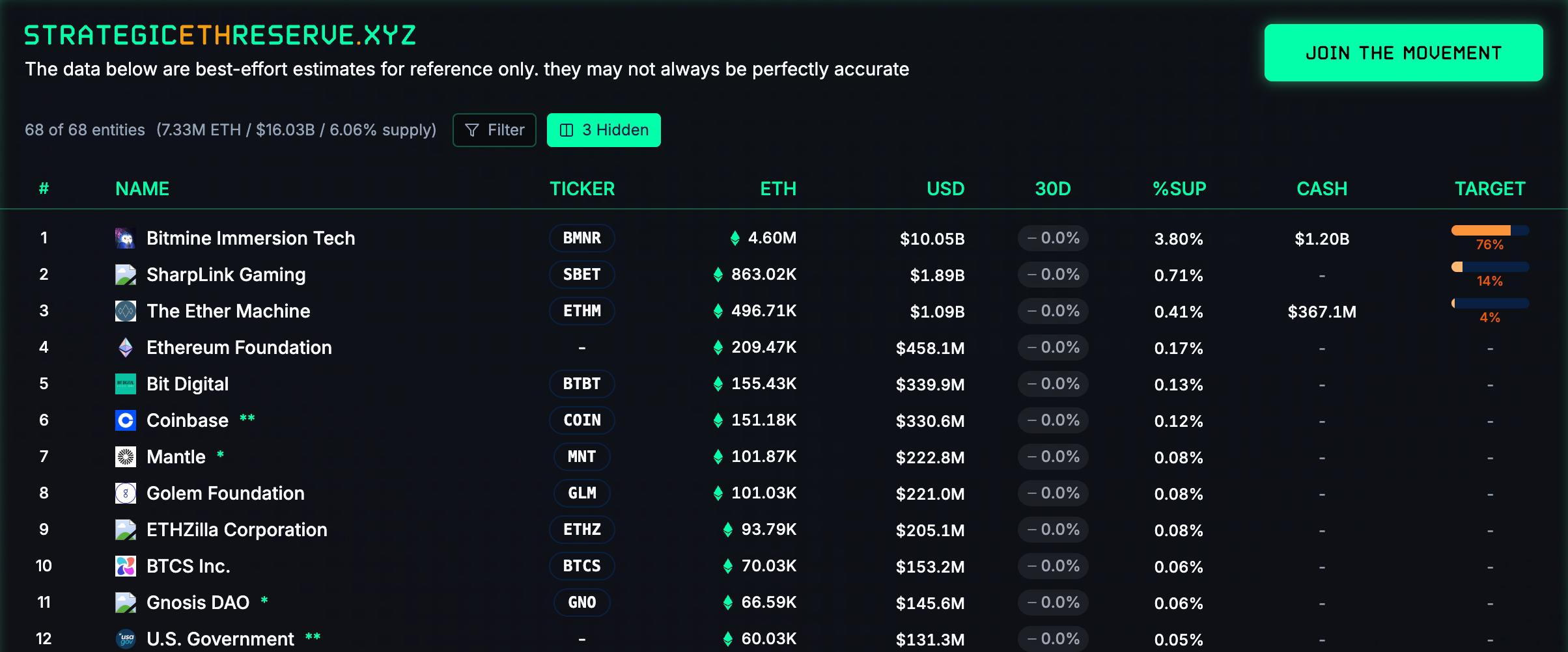

The first is float. ETH is being locked and absorbed faster than it is being created. Around 30% of all ETH is staked and illiquid. One corporate treasury, Bitmine, holds about 5.4 million ETH, roughly 4.5% of the entire supply, a figure Messari confirmed crossing five million this spring. This is the demand the fee bears cannot see, because it has nothing to do with revenue and everything to do with ETH being the reserve asset of the system. The honest counterweight: spot ETH ETFs bled about $216 million over ten days in late May, and ETH against Bitcoin just printed a year-to-date low near 0.027. Supply is being absorbed by treasuries and staking and released by ETFs at the same time. Which side wins is the real open question, and it is a far more useful one than “how much does the network burn.”

The second is the development moat, and this is where the bears are most wrong. Ethereum is not standing still while it loses fees. It is building what the next decade needs, in the open, faster than anyone else. The clearest proof landed in March, when Google’s Quantum AI team published a paper showing the cryptography behind Bitcoin and Ethereum could be broken with roughly twenty times fewer qubits than anyone thought. One of its co-authors was Justin Drake, an Ethereum Foundation researcher, alongside Stanford’s Dan Boneh.

Ethereum’s own people helped write the paper that exposes the threat, and Ethereum already has a concrete four-part plan to rip out and replace its vulnerable signatures, on a 2029 migration target shared with Google and Cloudflare, while the Bitcoin community is still arguing over whether the threat is even real and its ossification makes the fix unlikely. No cryptographically relevant quantum computer exists today, and the timeline is genuinely debated; Drake’s own odds are aggressive and personal. But the gap in readiness is not debated.

In January, Ethereum also shipped ERC-8004, an identity and reputation standard for AI agents, authored jointly by MetaMask, the Ethereum Foundation, Google, and Coinbase, paired with the x402 payment rail. Its privacy stack, Railgun, has shielded $4.5 billion and is being pulled directly into wallets by a Foundation initiative. The upgrades ship twice a year, on schedule.

Here is the correction the bulls need, though, because it is the same trap in reverse. None of that development reaches ETH through fees. We buried that idea three sections ago. It reaches the token, if it reaches it at all, by making ETH the unavoidable reserve and collateral of the venue where all of this gets built, and by keeping alive a cheap option that one of these threads, institutional settlement, autonomous agents, tokenized assets, eventually routes real value through the coin. That option is out of the money right now. It is also nearly free at today’s price.

[ETH/BTC ratio, Aug 2025 peak 0.0432 falling to ~0.027 now, with StanChart’s 0.08 target and the implied “monetary premium” prices drawn as dotted lines far above. Visualizes the gap between the models and the market. Source: market data / StanChart note.]

[The float war: stacked view of ETH absorbed (staking + treasuries) vs ETH released (ETF outflows + net issuance). Build once the net-float figure is locked. Source: strategicethreserve.xyz / Farside / ultrasound.money.]

The Same Mistake As The AI Trade, Pointed The Other Way

Mispriced has one recurring claim: markets get the technology right and the economics wrong.

In the last piece, on big tech’s AI profits, the error ran in one direction. The market priced the technology as real, which it is, and ignored that a chunk of the economics underneath was circular and partly imaginary. The gap was bearish. The narrative was richer than the cash.

ETH is the mirror image. The market is pricing the economics as broken, which they are, fees collapsed, burn dead, token inflating, and ignoring that the technology and the capex are compounding a position no competitor can touch. The gap is bullish, but only if you stop using the income statement to value an asset that was never an income statement in the first place.

Same mistake, opposite sign. With AI, people paid for economics that were not there. With ETH, people are refusing to pay for an asset because they are measuring the wrong economics. In both cases the capex told the truth before the price did. That is the whole job: find the place where what is being built and what is being paid for have come apart, and stand in the gap.

Price The Collateral, Not The Clearinghouse

There is a clean historical warning here, and it is not Amazon.

It is Cisco. Cisco was real infrastructure, the actual plumbing of the internet, and the dot-com market priced it like a religion, then left it roughly flat for two decades while the internet it powered remade the world. Real technology and a tradeable asset turned out to be two different bets. The bulls quoting Amazon should sit with Cisco for a minute.

But ETH inverts even that. The market is not overpricing the infrastructure. It is underpricing it, by measuring the wrong thing. Tom Dunleavy, in the noisiest bull thread of the spring, got exactly one thing right and the rest wrong: ETH is the collateral, not the clearinghouse. You do not value the world’s settlement layer by the toll it collects. You value the asset the system is forced to hold. But you do not arrive at a number by decree, the way his model and Etherealize’s both try to, and you do not earn the premium of dead money while rebuilding your own cryptography every single year.

So price the collateral, on demand, not on a formula.

What that gives you is not $250,000 and not zero. It is a slow repricing of the reserve asset of the chain that actually won, plus a free option on the institutions and the agents now arriving. Sustained growth, not a 100x. And it can stay mispriced for years, because nothing forces the gap shut on a schedule. I hold ETH on exactly that thesis, with my eyes open to exactly that risk.

The network already won. The token is the part still waiting. And that wait, not a six-figure fantasy and not a funeral, is where the mispricing actually lives.

---

Sources and full reference list: https://telegra.ph/Ethereum-Already-Won-Your-ETH-Didnt-References-06-03

---

Written by Udipta Basumatari. Nine years in crypto. Former CMO of two crypto-native startups, took the BWLD token to a $75 million market cap at launch, and, working solo and anonymously, launched a prediction-market token that reached a $3 million cap. Angel investor across multiple blockchain organizations and a long-time advocate for decentralized data ownership. I hold ETH long-term, which is rather the point: this is a bull reading his own bag honestly.

Mispriced asks one question: what is the market getting wrong, and what does the capex tell us that the narrative doesn’t? Subscribe for the next one.